What Makes Personal Finance Short-Form Videos Go Viral

Personal finance content dominates short-form video because it sits at the intersection of universal anxiety and universal aspiration - almost everyone worries about money and wants to do better with it. The top-performing videos in this niche share a consistent playbook: they lead with emotional permission, deliver concrete actionable frameworks, and use relatable identity framing to signal who the video is for before the first second is up. Creators who treat transparency as a strategy, not just a personality trait, consistently outperform those who default to generic advice.

Emotional Permission Hooks Outperform Information Hooks

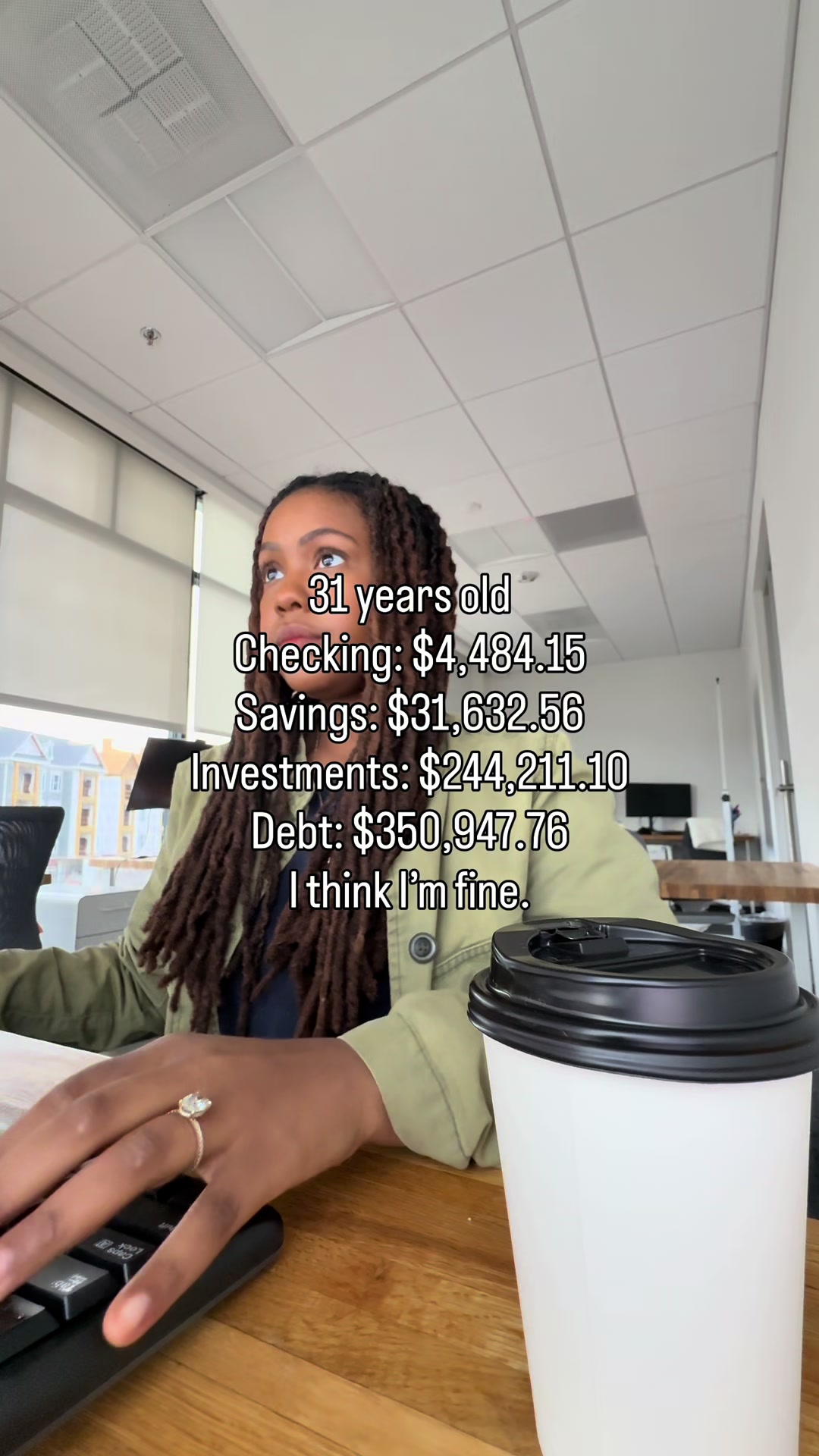

The highest outlier multiples in this dataset belong to videos that open by giving the viewer emotional permission before delivering any financial information. Phrases that normalize fear of checking your bank account, feeling behind for your age, or not knowing this stuff sooner all function as psychological unlocks rather than information promises. This works because the primary barrier to personal finance engagement is shame, not ignorance - once a creator dissolves shame in the first two seconds, the viewer is ready to learn. Pure information hooks like listing the top savings accounts perform solidly but cluster in the mid-tier outlier range, suggesting permission-first framing is the ceiling-raiser.

The Relatability-Credibility Balance Is the Core Format Decision

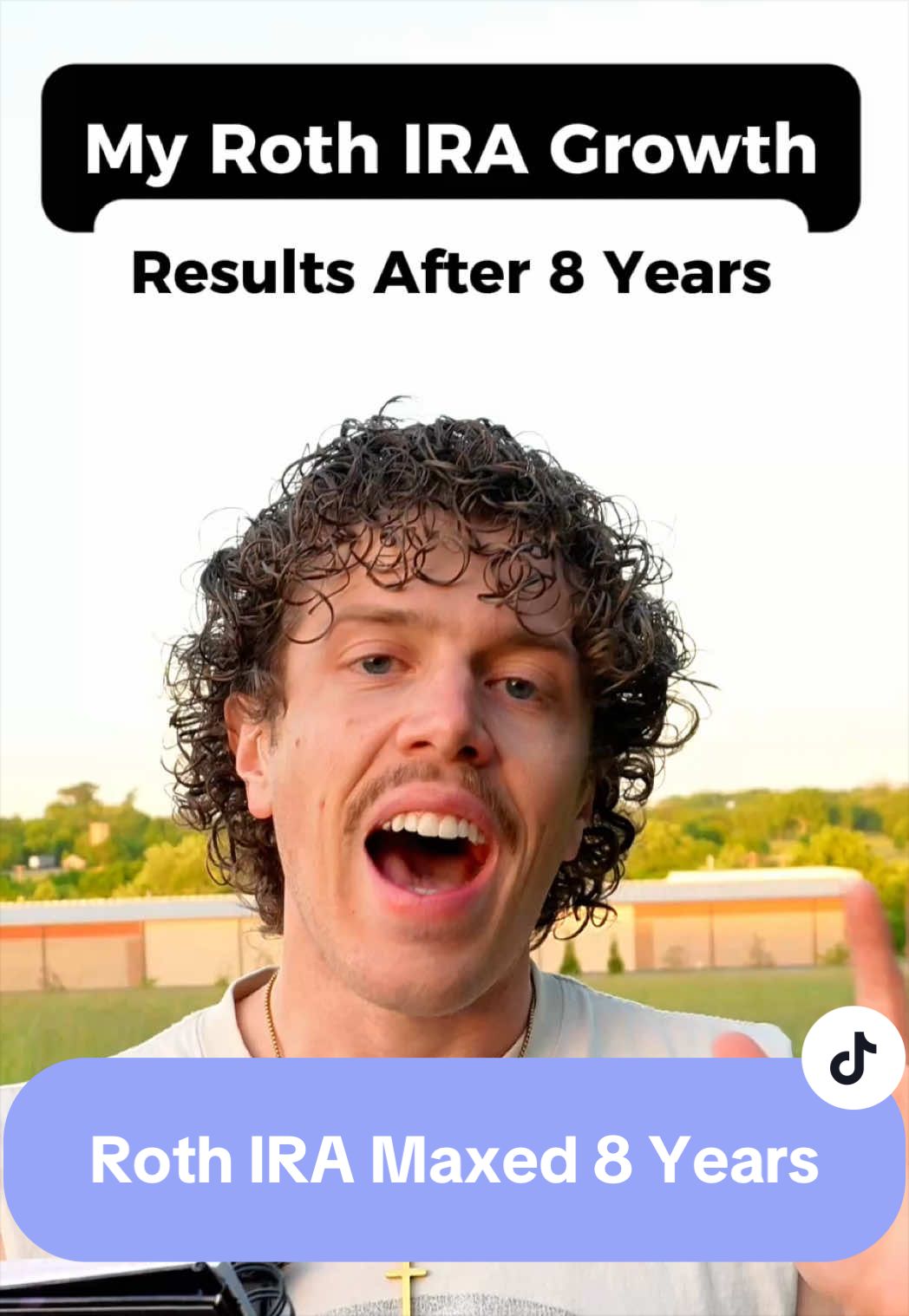

The best-performing videos in this niche carefully blend two signals that usually feel like opposites: 'I am just like you and figured this out' versus 'I have real expertise worth trusting.' Creators who lean too far into expertise come across as preachy and lose the algorithm; creators who lean too far into relatability lose credibility and watch time. The winning format establishes a personal narrative anchor in the hook, delivers structured financial information in the body, and closes with an outcome or result that validates both the creator and the viewer's decision to watch. Videos showing real account growth over multi-year timelines are a strong example of this balance done well.

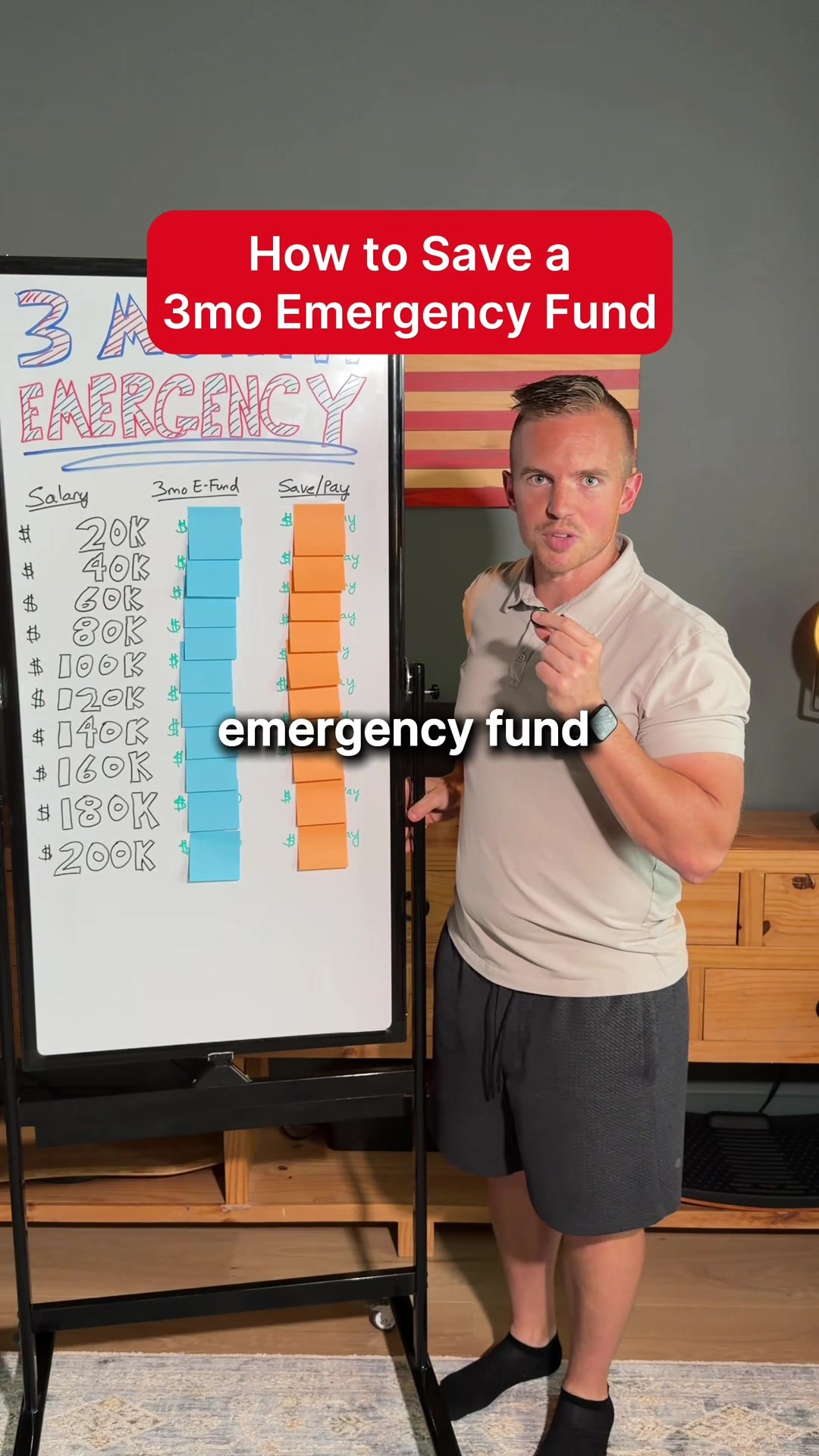

Numbered and Listicle Structures Drive Completion and Saves

Numbered frameworks, whether three tips, five-minute fixes, or step-by-step resets, appear repeatedly across the top performers because they set a clear cognitive contract with the viewer. When a viewer knows there are three things coming, they are more likely to watch to the end to collect all three, which boosts completion rate and signals quality to the algorithm. More importantly, listicle structures are the primary trigger for the save behavior on short-form platforms - viewers save finance videos they intend to act on later, and a clean numbered framework makes the video feel like a reusable reference rather than a one-time watch. Saves in this niche carry outsized algorithmic weight because they signal intent, not just entertainment.

Identity-Targeted Content Creates Tribal Amplification

Several of the strongest outliers are explicitly addressed to a specific demographic segment - women, young people, or people at a particular life stage - rather than a general audience. This targeting is a distribution strategy as much as a content strategy, because in-group viewers share identity-targeted content to their own networks as a form of social signaling. A video framed as finance tips for women gets shared by women to other women, creating organic referral loops that generalist finance content cannot replicate. The specificity also reduces the perceived gap between expert and viewer, making the advice feel more personally applicable and actionable.

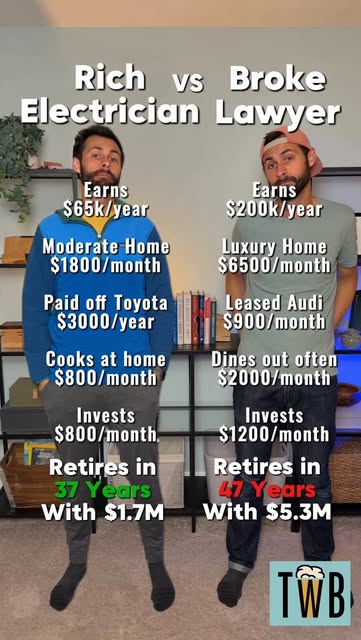

Comparative and Counterfactual Storytelling Hooks the Broadest Audiences

Some of the highest raw view counts in this dataset come from videos that use a side-by-side or 'what if' narrative structure, comparing two people, two life paths, or two financial choices and showing divergent outcomes over time. This format is powerful because it requires no prior financial knowledge to engage with - the viewer immediately understands the stakes through story rather than through data. Counterfactual and comparative structures also generate high comment volume because they invite the viewer to self-identify with one path or the other, which drives the kind of debate and discussion that platforms reward with extended distribution. These videos function more like financial parables than tutorials, and that broader narrative appeal explains their outsized raw reach.

Analysis generated by Reelyze from 20 top-performing personal finance videos.